Introduction to AR and MA models

Contents

Introduction to AR and MA models¶

Time series models¶

aim to capture complex temporal dependence

build by combining processes with simple dependence structure - innovations

Innovations¶

white noise

martingale difference

iid

Linear time series models¶

The time series \(\mathbf{z}\) and the innovation \(\boldsymbol \varepsilon\) are linearly related

or more generally, the transformation \(\boldsymbol \varepsilon \rightarrow \mathbf{z}\) is affine

with Gaussian innovations \(p(\boldsymbol \varepsilon) \sim \mathcal{N}(\boldsymbol 0, \sigma^2\mathbf{I})\)

Moving Average (MA) models¶

MA(1)¶

Stationarity conditions¶

constant mean?

constant variance?

constant covariances?

for lag \(h=1\)

for lag \(h\geq 2\)

import warnings

warnings.simplefilter("ignore", FutureWarning)

import matplotlib.pyplot as plt

import numpy as np

from statsmodels.tsa.arima_process import arma_acovf

from scipy.linalg import toeplitz

from matplotlib import rc

rc('font',**{'family':'serif','serif':['Palatino']})

rc('text', usetex=True)

plt.rcParams.update({'ytick.left' : True,

"xtick.bottom" : True,

"ytick.major.size": 0,

"ytick.major.width": 0,

"xtick.major.size": 0,

"xtick.major.width": 0,

"ytick.direction": 'in',

"xtick.direction": 'in',

'ytick.major.right': False,

'xtick.major.top': True,

'xtick.top': True,

'ytick.right': True,

'ytick.labelsize': 18,

'xtick.labelsize': 18

})

np.random.seed(12345)

def correlation_from_covariance(covariance):

v = np.sqrt(np.diag(covariance))

outer_v = np.outer(v, v)

correlation = covariance / outer_v

correlation[covariance == 0] = 0

return correlation

def show_covariance(cov_mat, process_name):

K = cov_mat.shape[0]

fig, ax = plt.subplots(nrows=1, ncols=1, figsize=(20,8))

c = ax.imshow(cov_mat,

cmap="magma_r",

)

#c = ax.pcolormesh(Sigma, edgecolors='k', linewidth=.01, cmap='inferno_r')

#ax = plt.gca()

#ax.set_aspect('equal')

#ax.invert_yaxis()

plt.colorbar(c);

ax.set_xticks(range(0,K))

ax.set_xticklabels(range(1, K+1));

ax.set_yticks(range(0,K))

ax.set_yticklabels(range(1, K+1));

ax.set_title(f'Covariance {process_name}', fontsize=24)

plt.subplots_adjust(wspace=-0.7)

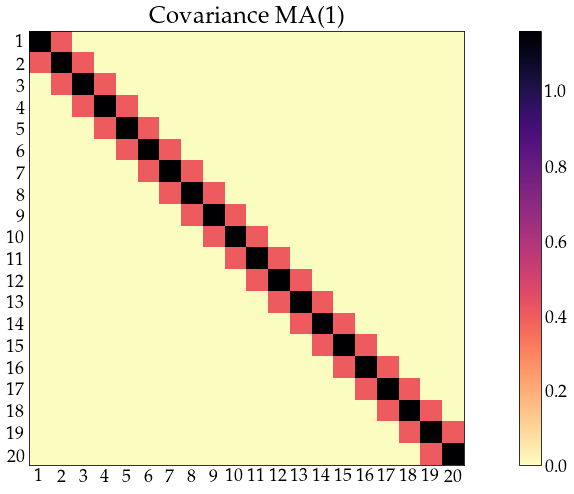

n_obs = 20

arparams = np.array([0])

maparams = np.array([.4])

ar = np.r_[1, -arparams] # add zero-lag and negate

ma = np.r_[1, maparams] # add zero-lag

sigma2=np.array([1])

acov_ma1 = arma_acovf(ar=ar, ma=ma, nobs=n_obs, sigma2=sigma2)

Sigma_ma1 = toeplitz(acov_ma1)

corr_ma1 = correlation_from_covariance(Sigma_ma1)

show_covariance(cov_mat=Sigma_ma1, process_name='MA(1)')

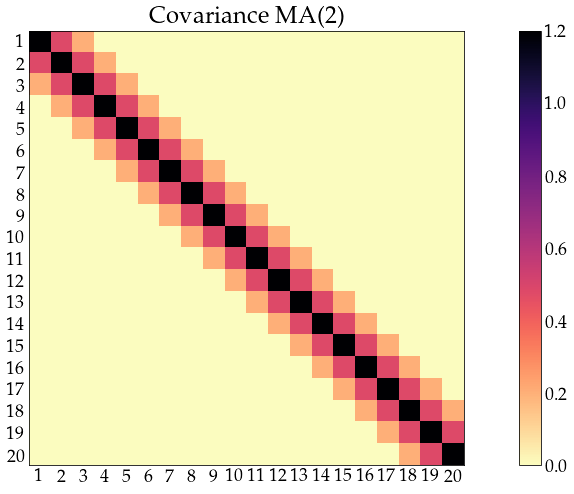

n_obs = 20

arparams = np.array([0])

maparams = np.array([.4, .2])

ar = np.r_[1, -arparams] # add zero-lag and negate

ma = np.r_[1, maparams] # add zero-lag

sigma2=np.array([1])

acov_ma2 = arma_acovf(ar=ar, ma=ma, nobs=n_obs, sigma2=sigma2)

Sigma_ma2 = toeplitz(acov_ma2)

corr_ma2 = correlation_from_covariance(Sigma_ma2)

show_covariance(cov_mat=Sigma_ma2, process_name='MA(2)')

need (at least) MA(q) to have dependence between \(z_t\) and \(z_{t+q}\)

not parsimonious (\(q+1\) parameters to estimate)

Autoregressive (AR) models¶

AR(1)¶

initial values \(z_0\)¶

known constant, e.g. \(z_0=0\)

unknown constant, to be estimated

unknown random variable, independent from \(\varepsilon_t\), e.g. \(z_0 \sim \mathcal{N}(0, \sigma^2_0)\), \(\sigma_0\) to be estimated

unknown random variable, independent from \(\varepsilon_t\) e.g. \(z_0 \sim \mathcal{N}(0, \frac{\sigma^2}{1-\alpha^2})\)

equivalent to \(z_0 = \frac{\varepsilon_0}{\sqrt{1-\alpha^2}}\), with \(\varepsilon_0 \sim \mathcal{N}(0, \sigma^2)\)

Stationarity conditions¶

constant variance (\(\sigma^2_{z_t} = \sigma^2_{z_{t+k}} = \gamma(0) \)):

since \(\sigma^2 > 0\), \(\alpha \neq \pm 1\)

constant mean (\(\operatorname E z_t = \operatorname E z_{t+k} = \mu_{z} \))

since \(\alpha \neq 1\)

constant covariances (\(\operatorname{cov}(z_t, z_{t+h}) = \operatorname E (z_t z_{t+h}) = \gamma(h)\))

covariance is time-invariant

correlation is time-invariant

(stability condition) for \(\operatorname{corr}(z_t, z_{t+h}) \rightarrow 0\) as \(h \rightarrow \infty\)

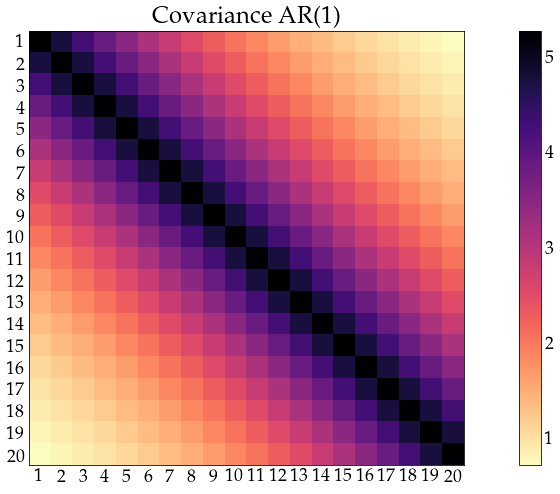

n_obs = 20

arparams = np.array([0.9])

maparams = np.array([0])

ar = np.r_[1, -arparams] # add zero-lag and negate

ma = np.r_[1, maparams] # add zero-lag

sigma2=np.array([1])

acov_ar1 = arma_acovf(ar=ar, ma=ma, nobs=n_obs, sigma2=sigma2)

Sigma_ar1 = toeplitz(acov_ar1)

corr_ar1 = correlation_from_covariance(Sigma_ar1)

show_covariance(cov_mat=Sigma_ar1, process_name='AR(1)')

MA and AR processes in Python¶

from statsmodels.tsa.arima_process import ArmaProcess

# create a MA(1) model

theta = np.array([.4])

ar = np.r_[1] # the coefficient on $z_t$

ma = np.r_[1, theta]

ma1_process = ArmaProcess(ar, ma)

print(ma1_process)

ArmaProcess

AR: [1.0]

MA: [1.0, 0.4]

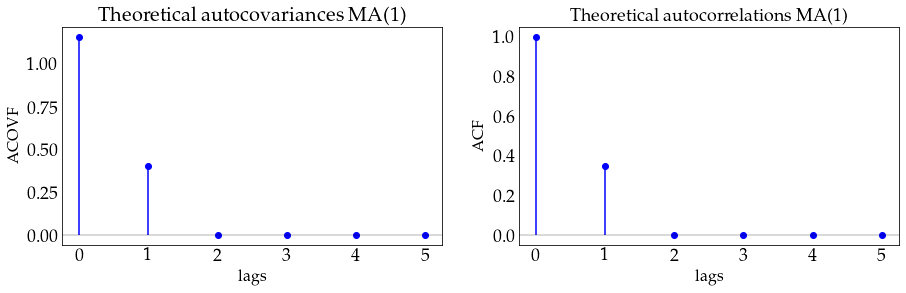

autocovariances and autocorrelations (MA models)¶

ma1_process.acovf(3)

array([1.16, 0.4 , 0. ])

#compare to analytical result

print([1*(1+theta**2), theta])

[array([1.16]), array([0.4])]

def plot_autocov(process, nlags, process_name):

lags = np.arange(nlags+1)

acovf_x = process.acovf(nlags+1)

acf_x = process.acf(nlags+1)

fig, (ax1, ax2) = plt.subplots(nrows=1, ncols=2, figsize=(15, 4))

ax1.vlines(lags, [0], acovf_x, color='b')

ax1.scatter(lags, acovf_x, marker='o', c='b')

ax1.axhline(color='black', linewidth=.3)

ax1.set_xticks(lags)

ax1.set_xlabel('lags', fontsize=16)

ax1.set_ylabel('ACOVF', fontsize=16)

ax1.set_title(f'Theoretical autocovariances {process_name}', fontsize=20)

ax2.vlines(lags, [0], acf_x, color='b')

ax2.scatter(lags, acf_x, marker='o', c='b')

ax2.axhline(color='black', linewidth=.3)

ax2.set_xticks(lags)

ax2.set_xlabel('lags', fontsize=16)

ax2.set_ylabel('ACF', fontsize=16)

ax2.set_title(f'Theoretical autocorrelations {process_name}', fontsize=18)

def plot_sample(z, process_name):

fig, ax = plt.subplots(figsize=(12,4))

ax.plot(z, c='black')

ax.set_xlabel('time', fontsize=16)

ax.set_title(f'{process_name}', fontsize=18)

plot_autocov(process=ma1_process, nlags=5, process_name='MA(1)')

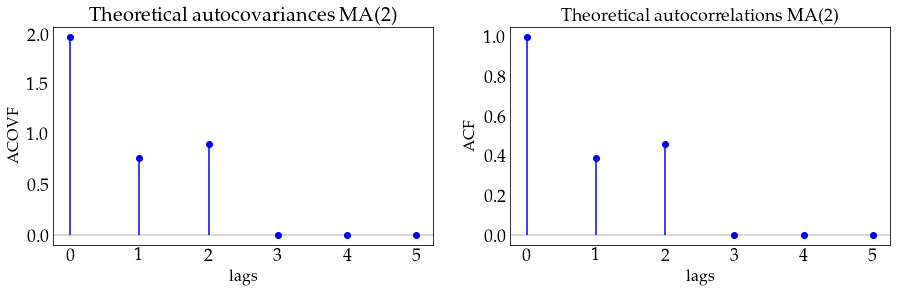

# define a MA(2) model

theta = np.array([.4, .9])

ar = np.r_[1] # the coefficient on $z_t$

ma = np.r_[1, theta]

ma2_process = ArmaProcess(ar, ma)

plot_autocov(process=ma2_process, nlags=5, process_name='MA(2)')

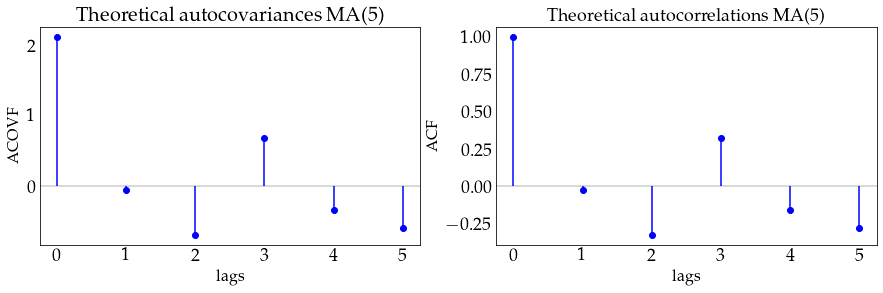

# define a MA(5) model

theta = np.array([.4, -.7, .3, -.1, -.6])

ar = np.r_[1] # the coefficient on $z_t$

ma = np.r_[1, theta]

ma5_process = ArmaProcess(ar, ma)

plot_autocov(process=ma5_process, nlags=5, process_name='MA(5)')

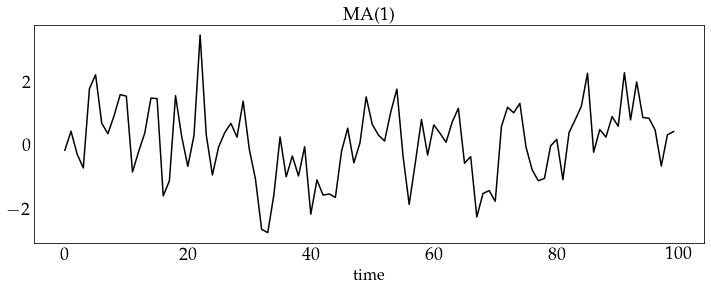

# generate a sample from the MA(1) model and plot it

z_ma1 = ma1_process.generate_sample(100)

plot_sample(z_ma1, process_name='MA(1)')

# generate a sample from the MA(2) model and plot it

z_ma2 = ma2_process.generate_sample(100)

plot_sample(z_ma2, process_name='MA(2)')

# generate a sample from the MA(5) model and plot it

z_ma5 = ma5_process.generate_sample(100)

plot_sample(z_ma5, process_name='MA(5)')

autocovariances and autocorrelations (AR models)¶

alpha = .8 # coefficient on z(t-1)

ar = np.r_[1, -alpha]

ma = np.r_[1] # coefficient on e(t)

ar1_process = ArmaProcess(ar, ma)

print(ar1_process)

ArmaProcess

AR: [1.0, -0.8]

MA: [1.0]

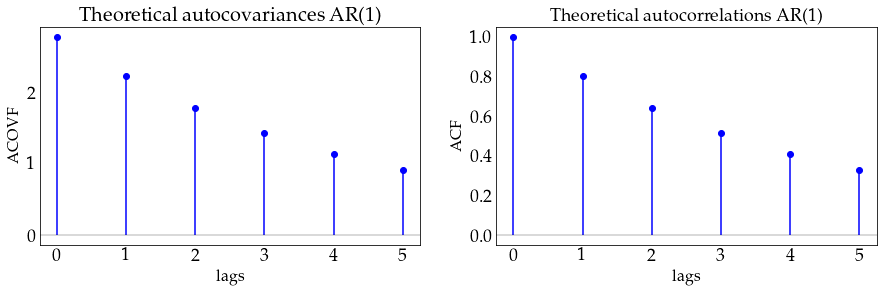

ar1_process.acovf(3)

array([2.77777778, 2.22222222, 1.77777778])

#compare to analytical result

sigma=1

print([sigma**2 / (1-alpha**2), \

alpha*sigma**2/(1-alpha**2), \

alpha**2*sigma**2/(1-alpha**2)

])

[2.7777777777777786, 2.222222222222223, 1.7777777777777788]

plot_autocov(process=ar1_process, nlags=5, process_name='AR(1)')

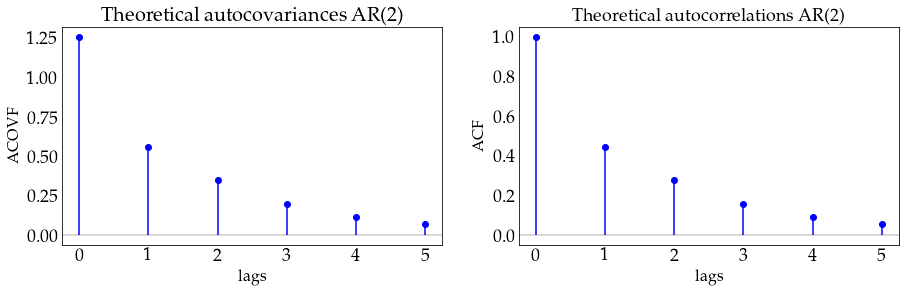

alpha = np.array([.4, .1])

ar = np.r_[1, -alpha] # the coefficient on $z_t$

ma = np.r_[1]

ar2_process = ArmaProcess(ar, ma)

plot_autocov(process=ar2_process, nlags=5, process_name='AR(2)')

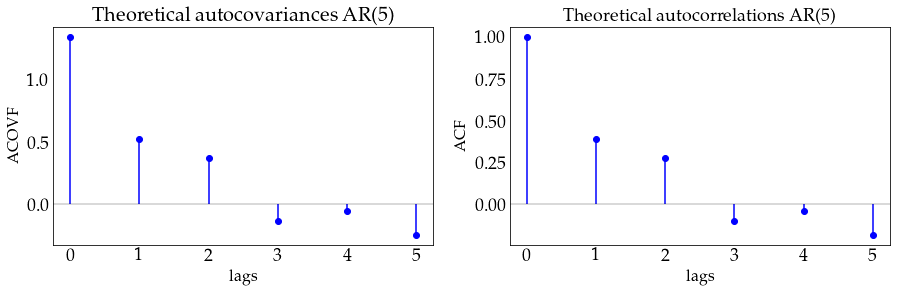

alpha = np.array([.4, .2, -.3, .1, -.1])

ar = np.r_[1, -alpha] # the coefficient on $z_t$

ma = np.r_[1]

ar5_process = ArmaProcess(ar, ma)

plot_autocov(process=ar5_process, nlags=5, process_name='AR(5)')

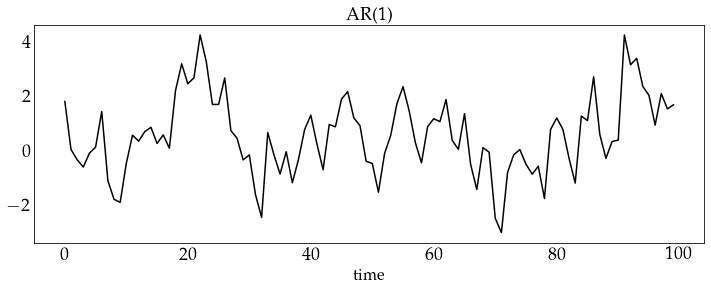

z_ar1 = ar1_process.generate_sample(100)

plot_sample(z_ar1, process_name='AR(1)')

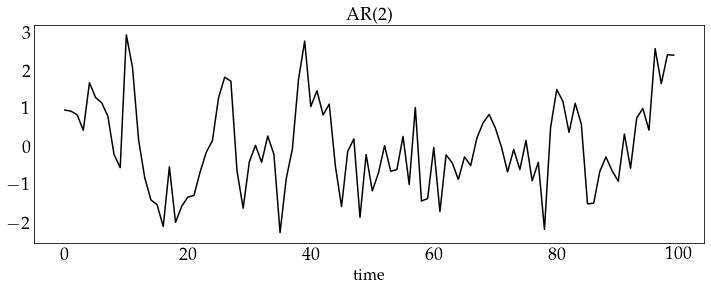

z_ar2 = ar2_process.generate_sample(100)

plot_sample(z_ar2, process_name='AR(2)')

z_ar5 = ar5_process.generate_sample(100)

plot_sample(z_ar5, process_name='AR(5)')