Non-stationarity and unit root processes

Contents

Non-stationarity and unit root processes¶

import warnings

warnings.simplefilter("ignore", FutureWarning)

from statsmodels.tsa.deterministic import DeterministicProcess

import pandas as pd

import numpy as np

from numpy.random import default_rng

from statsmodels.tsa.arima_process import arma_acovf, ArmaProcess

from statsmodels.tsa.arima.model import ARIMA

import matplotlib.pyplot as plt

import statsmodels.api as sm

gen = default_rng(1)

import seaborn as sns

sns.set_theme()

sns.set_context("notebook")

Why need stationarity?¶

stationarity is a form of constancy of the properties of the process (mean, variance, autocovariances)

needed in order to be able to learn something about those properties

Many macroeconomic time series are non-stationary

#df = pd.read_excel('nama_10_gdp__custom_2373104_page_spreadsheet.xlsx',

# sheet_name='Sheet 1',

# skiprows=range(9), usecols=[0,1], names=['year', 'GDP'], index_col=0, parse_dates=True,

# ).loc['1995':'2021']

#df = df.astype('float')

#data = np.log(df['GDP'])

#title='Real GDP, Euro Area'

#ylabel='natural log of millions of euro'

#fig = data.plot(figsize=(10,3), title=title,ylabel=ylabel)

#plt.savefig('images/rGDPea.png')

ARMA(p, q)¶

in lag operator notation

ARMA(p, q) is stationary if the AR§ part is stationary, i.e. if all roots of

are outside the unit circle (\(|x|>1\))

a non-stationary process with one root \(x=1\) and the other roots \(|x|>1\) is called a unit root process

if \(z_t\) is an unit root process, \(\Delta z_t = z_t - z_{t-1} = (1-L) z_t\) is stationary

and if all roots of

are outside the unit circle (\(|x|>1\))

the AR part

a non-stationary process whose first difference is stationary is called integrated of order one (\(I(1)\))

why “integrated”:

\(z_t\) is the sum (integral) of a process (is an “integrated” process) starting from some initialization \(z_0\)

\(\sum_{j=1}^{t} u_j\) refered to as a stochastic trend

\(\Delta z_t\) is \(I(0)\) (stationary, no need to difference)

a non-stationary process which requres double difference to be stationary is called integrated of order two (\(I(2)\))

if \(z_t\) is \(I(2)\) then \(\Delta^2 z_t = (1-L)^2 z_t\) is \(I(0)\)

etc for \(I(d)\).

if \(z_t\) is \(I(d)\) then \(\Delta^d\) is \(I(0)\)

\(d\) is the order of integration

if we difference a stationary process, we get another stationary process. However, no differencing was required to achieve stationarity

stationary process whose cumulative sum is also stationary, are called overdifferenced, and denoted with \(I(-1)\)

example:

\(z_t\) is stationary but so is \(\varepsilon_t\)

\(z_t\) is \(I(-1)\)

non-invertible MA part

another example:

is \(I(-1)\)

linear time trend (deterministic trend)

\(z_t\) is called trend-stationary process

in the sense that it is non-random

more generally:

where \(\mathbf{x_t}\) are known constants

is stationary

Gaussian MLE¶

and, if \(\nu_t\) is stationary Gaussian time series process

we have

where

for example, if \(z_t = \delta_0 + \delta_1 t + \nu_t\), the \(t\)-th row of \(\boldsymbol X\) is \([1, t]\)

Models with time trend in Python¶

Generate \(\boldsymbol X\) for

\(T \times 2\) matrix with \(t\)-th row given by \([1, t]\)

from statsmodels.tsa.deterministic import DeterministicProcess

T = 500

index = pd.RangeIndex(0, T)

det_proc = DeterministicProcess(index, constant=True, order=1) # constant and a linear (1 order) trend

X = det_proc.in_sample()

X.head()

| const | trend | |

|---|---|---|

| 0 | 1.0 | 1.0 |

| 1 | 1.0 | 2.0 |

| 2 | 1.0 | 3.0 |

| 3 | 1.0 | 4.0 |

| 4 | 1.0 | 5.0 |

# constant and time trend part

delta = np.array([3, .1])

exog = X.values@delta

\(\nu_t\) as ARMA(1,1) process

alpha = np.array([.8])

beta = np.array([0.1])

ar = np.r_[1, -alpha] # coefficient on z(t) and z(t-1)

ma = np.r_[1, beta] # coefficients on e(t) and e(t-1)

arma11_process = ArmaProcess(ar, ma)

nu = arma11_process.generate_sample(T, distrvs=gen.normal)

z = exog + nu

Option 1 Estimate indicating constant and time trend

arma_model = ARIMA(z, order=(1, 0, 1), trend="ct")

arma_results = arma_model.fit()

print(arma_results.summary())

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 500

Model: ARIMA(1, 0, 1) Log Likelihood -733.673

Date: Mon, 28 Mar 2022 AIC 1477.345

Time: 10:48:25 BIC 1498.418

Sample: 0 HQIC 1485.614

- 500

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 3.0500 0.512 5.954 0.000 2.046 4.054

x1 0.0992 0.002 57.573 0.000 0.096 0.103

ar.L1 0.7971 0.035 22.981 0.000 0.729 0.865

ma.L1 0.0650 0.057 1.142 0.253 -0.047 0.176

sigma2 1.1054 0.073 15.235 0.000 0.963 1.248

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 0.28

Prob(Q): 1.00 Prob(JB): 0.87

Heteroskedasticity (H): 1.20 Skew: -0.01

Prob(H) (two-sided): 0.24 Kurtosis: 2.89

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Option 2 Estimate providing exogenous regressors

arma_model2 = ARIMA(z, exog=X, order=(1, 0, 1), trend="n")

arma_results2 = arma_model2.fit()

print(arma_results2.summary())

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 500

Model: ARIMA(1, 0, 1) Log Likelihood -733.673

Date: Mon, 28 Mar 2022 AIC 1477.345

Time: 10:48:29 BIC 1498.418

Sample: 0 HQIC 1485.614

- 500

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 3.0500 0.512 5.954 0.000 2.046 4.054

trend 0.0992 0.002 57.573 0.000 0.096 0.103

ar.L1 0.7971 0.035 22.981 0.000 0.729 0.865

ma.L1 0.0650 0.057 1.142 0.253 -0.047 0.176

sigma2 1.1054 0.073 15.235 0.000 0.963 1.248

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 0.28

Prob(Q): 1.00 Prob(JB): 0.87

Heteroskedasticity (H): 1.20 Skew: -0.01

Prob(H) (two-sided): 0.24 Kurtosis: 2.89

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Difference-stationary vs trend-stationary¶

trend-stationary if \(\nu_t\) is stationary

difference-stationary if \(\nu_t\) is a unit root process

\(\nu_t\) is a unit root process if in

one of the roots of

is \(x=1\), and the other roots are \(|x|>1\)

all \(p\) roots of

are \(|x|>1\)

\(\Delta \nu_t = (1-L)\nu_t\) is a stationary ARMA(p, q) process

Difference-stationary process¶

\( \nu_t\) is an ARIMA(p, 1, q) process

\(z_t\) is an ARIMAX(p, 1, q) process (ARIMA with exogenous part - constant and time trend)

\(\Delta z_t\) is an ARMAX(p, q) process (ARMA with exogenous part - constant)

model \(z\) as regression model with ARIMA errors

Difference between trend- and difference-stationary models¶

example

at \(t+h\)

forecast at \(t\):

if \(|\alpha|<1\), as \(h\rightarrow \infty\), \(\alpha^h \rightarrow 0\)

For trend-stationary processes:

the long-run forecast is the unconditional mean of \(z_t\) (mean reversion)

the long-run forecast is independent of \(z_t\)

shocks to \(z_t\) have temporary impact (transitory)

if \(\alpha=1\),

For difference-stationary processes:

the value of \(z_t\) has a permanent effect on all future forecasts

shocks to \(z_t\) have permanent effects

\(z_t\) is expected to grow by \(\delta_1\) every period

Martingale process¶

if for \(\{z_t\}_{-\infty}^{\infty}\)

\(z_t\) is a martingale process, and \(\Delta z_t\) is a martingale difference process

unlike a random walk, martingale process allows for heteroskedasticity or conditional heteroskedasticity

Beveridge-Nelson decomposition¶

Every difference-stationary process can be written as a sum of a random walk and a stationary component

the effect of innovations (shocks) can be decomposed into permanent and transitory effects

ARIMA(p,1,q)

\(\alpha(L)\) is invertible. Why?

equivalently (by invertability of \(\alpha(L)\))

(a bit of magic here…)

Since 1 is a root of the polinomial

it can be witten as

and

where

denote \(z_t^p = (1-L)^{-1}\delta_1 + (1-L)^{-1}\phi(1)\varepsilon_t\)

then,

Therefore

\(z^p_t\) - permanent component (trend)

\(z^s_t\) - transitory component (cycle)

\(\varepsilon_t\) has a permanent impact on \(z_t\) through \(z_t^p\)

\(\varepsilon_t\) has a transitory impact on \(z_t\) through \(z_t^s\)

relative importance of permanent/transitory impact depends on the value of \(\phi(1)\)

example ARIMA(0,1,1)

Random walk with a drift model:¶

Beveridge-Nelson decomposition¶

Every difference-stationary processes can be written as a sum of a random walk and a stationary component

many macro variables are well represented by ARIMA(p,1,q) models

every ARIMA(p,1,q) model has a random walk stochastic trend

the growth in macro variables can be characterized by stochastic trends

Forecasting integrated variables¶

if \(z_t\) is \(I(1)\), we estimate and forecast using \(\Delta z_t\)

from the forecasts of \(\Delta z_{t+i}\), \(i=1, 2, \cdots, h\)

Detecting stochastic trends by unit root test¶

Unit root tests are one-sided tests:

\(H_0\): unit root

\(H_1\): stationary

Augmented Dickey–Fuller test¶

Consider AR(2) process:

re-write as

and

For AR(2) process, unit root means that \(x=1\) is a solution to

i.e

Therefore, testing for unit root is equivalent to testing that \(\rho=0\) in

In general AR§ model for \(z_t\)

testing for unit root is equivalent to testing that \(\rho=0\)

in (5) the \(H_1\) is that \(z_t\) is a stationary mean 0 AR§ process

to test for unit root agains \(H_1\) that \(z_t\) is a stationary around a constant (\(\neq 0\)) mean, estimate

to test for unit root agains \(H_1\) that \(z_t\) is a stationary around a deterministic linear time trend (trend-stationary)

appropriate for series that exhibit growth over the long run

The test for unit root is a test of \(\rho=0\) (unit root) against the alternative of \(\rho<0\) (stationary)

The asymptotic distribution of the test statistic for \(\rho\) is non-standard.

The critical values of the test statistics are obtained by Monte Carlo simulations, and depend of whether constant and time trend are included

The null hypothesis of a unit root is rejected when value of the test statistics is below the critical value.

If the null hypothesis cannot be rejected, \(z_t\) should be differenced prior to estimation

ADF test in Python¶

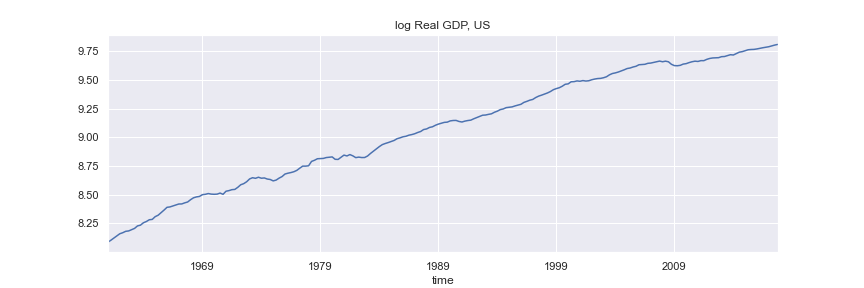

df = pd.read_stata(r"C:\Users\eeu227\Documents\PROJECTS\econ108-repos\econ108-practice\EconometricsData\FRED-QD\FRED-QD.dta")

rgdp = df[['time', 'gdpc1']].set_index('time')['1961q1':].rename(columns={'gdpc1': 'rGDP'})

rgdp = np.log(rgdp)

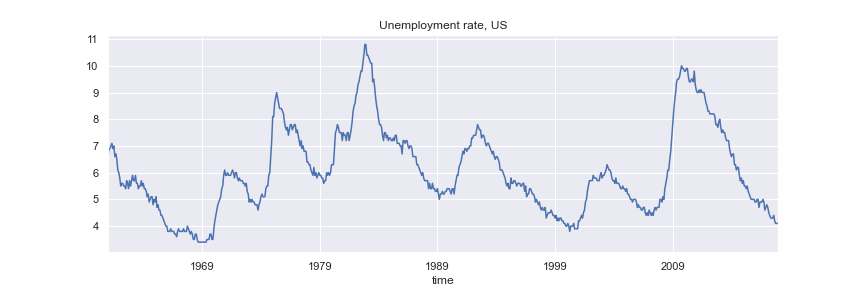

df = pd.read_stata(r"C:\Users\eeu227\Documents\PROJECTS\econ108-repos\econ108-practice\EconometricsData\FRED-MD\FRED-MD.dta")

unemp = df[['time', 'unrate']].set_index('time')['1961-01':]

df = pd.read_stata(r"C:\Users\eeu227\Documents\PROJECTS\econ108-repos\econ108-practice\EconometricsData\FRED-MD\FRED-MD.dta")

cpi = np.log(df[['time', 'cpiaucsl']].set_index('time')['1961-01':])

dcpi = (cpi.diff(12)*100).dropna()

Real GDP¶

#fig = rgdp.plot(figsize=(12,4), title='log Real GDP, US', legend=False)

#plt.savefig('images/rGDPus.png')

from statsmodels.tsa.stattools import adfuller

def get_adfresults(dftest):

dfoutput = pd.Series(

dftest[0:4],

index=[

"Test Statistic",

"p-value",

"#Lags Used",

"Number of Observations Used",

],

)

for key, value in dftest[4].items():

dfoutput[f"Critical Value ({key})"] = value

return dfoutput

ADF with constant and trend, 4 lags

dftest = adfuller(rgdp, maxlag=4, autolag=None, regression='ct')

dftest

(-2.0141544954585036,

0.5937024444875985,

4,

223,

{'1%': -3.9999506167815206,

'5%': -3.4303636888103926,

'10%': -3.138725564735756})

get_adfresults(dftest)

Test Statistic -2.014154

p-value 0.593702

#Lags Used 4.000000

Number of Observations Used 223.000000

Critical Value (1%) -3.999951

Critical Value (5%) -3.430364

Critical Value (10%) -3.138726

dtype: float64

Automatically determine optimal number of lags using AIC

dftest = adfuller(rgdp, autolag="AIC", regression='ct')

get_adfresults(dftest)

Test Statistic -2.157741

p-value 0.513651

#Lags Used 2.000000

Number of Observations Used 225.000000

Critical Value (1%) -3.999579

Critical Value (5%) -3.430185

Critical Value (10%) -3.138621

dtype: float64

Unemployment Rate¶

#fig = unemp.plot(figsize=(12,4), title='Unemployment rate, US', legend=False)

#plt.savefig('images/UNus.png')

dftest = adfuller(unemp, autolag='AIC', regression='c')

get_adfresults(dftest)

Test Statistic -2.996063

p-value 0.035264

#Lags Used 12.000000

Number of Observations Used 671.000000

Critical Value (1%) -3.440133

Critical Value (5%) -2.865857

Critical Value (10%) -2.569069

dtype: float64

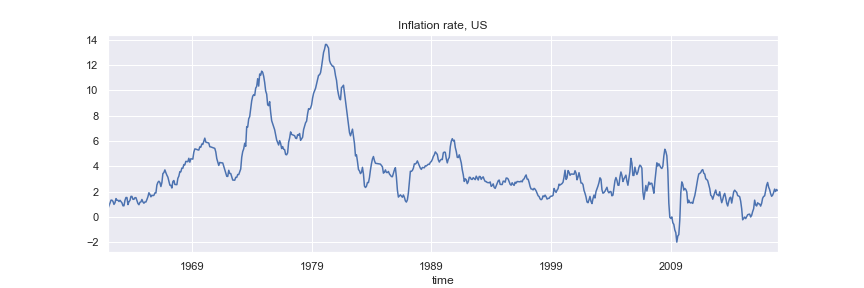

Consumer Price Inflation¶

#fig = dcpi.plot(figsize=(12,4), title='Inflation rate, US', legend=False)

#plt.savefig('images/dCPIus.png')

dftest = adfuller(dcpi, autolag='AIC', regression='c')

get_adfresults(dftest)

Test Statistic -2.804916

p-value 0.057575

#Lags Used 15.000000

Number of Observations Used 656.000000

Critical Value (1%) -3.440358

Critical Value (5%) -2.865956

Critical Value (10%) -2.569122

dtype: float64

ADF test using ARCH¶

from arch.unitroot import ADF

adf = ADF(rgdp, trend="ct")

adf.summary()

| Test Statistic | -2.158 |

| P-value | 0.514 |

| Lags | 2 |

Trend: Constant and Linear Time Trend

Critical Values: -4.00 (1%), -3.43 (5%), -3.14 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

Examine the regression results¶

reg_res = adf.regression

print(reg_res.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.176

Model: OLS Adj. R-squared: 0.161

Method: Least Squares F-statistic: 11.76

Date: Mon, 28 Mar 2022 Prob (F-statistic): 1.13e-08

Time: 16:43:14 Log-Likelihood: 786.27

No. Observations: 225 AIC: -1563.

Df Residuals: 220 BIC: -1545.

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Level.L1 -0.0217 0.010 -2.158 0.032 -0.041 -0.002

Diff.L1 0.2365 0.065 3.611 0.000 0.107 0.366

Diff.L2 0.1917 0.066 2.923 0.004 0.062 0.321

const 0.1848 0.083 2.231 0.027 0.022 0.348

trend 0.0001 7.5e-05 1.935 0.054 -2.67e-06 0.000

==============================================================================

Omnibus: 17.613 Durbin-Watson: 1.994

Prob(Omnibus): 0.000 Jarque-Bera (JB): 56.070

Skew: -0.116 Prob(JB): 6.68e-13

Kurtosis: 5.435 Cond. No. 2.21e+04

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 2.21e+04. This might indicate that there are

strong multicollinearity or other numerical problems.

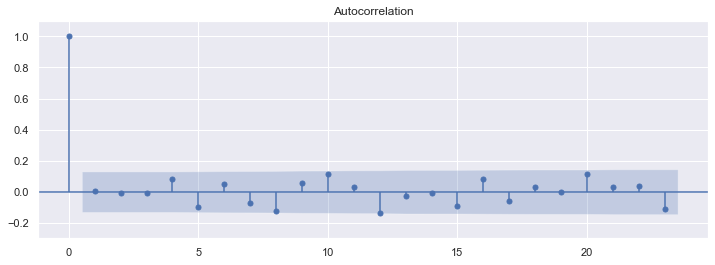

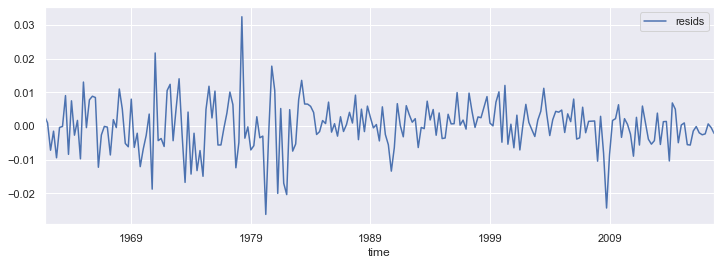

Examine the regression residuals¶

resids = pd.DataFrame(reg_res.resid)

resids.index = rgdp.index[3:]

resids.columns = ["resids"]

fig = resids.plot(figsize=(12,4))

fig, ax = plt.subplots(figsize=(12,4))

fig = sm.graphics.tsa.plot_acf(reg_res.resid, lags=23, ax=ax)

ax.set_ylim([-0.3, 1.1])

(-0.3, 1.1)